You’re two weeks into Series A diligence. Your lead investor’s counsel has sent a 40-item request list and you can produce clean answers to about half of it. The rest requires work like tightening IP assignments, reconciling inconsistent SAFE terms, or producing board consents that were never formally documented.

You call your lawyer. The quote comes back: $35,000 to $50,000, billed hourly, with a caveat that the number could move “depending on complexity.” You have no way to evaluate whether that number is fair, what's driving it, or what “depending on complexity” actually means in dollars.

You have no framework for understanding what the price reflects. And that problem started long before this phone call, in the engagement letter you signed without reading closely six months ago.

What you’re paying for versus what you’re getting

Most startup legal bills are built on inputs. A partner at a Biglaw firm might bill at $1,350 an hour, a senior associate at $1,100, a junior associate at $750. The rates vary by market and firm, but the structure is consistent: a blended rate that reflects the firm’s staffing decisions and overhead, not the value of the deliverable to you. And the work is often being done by someone two or three years out of law school who is still learning the mechanics of a SAFE conversion.

The billing model shapes the staffing model, which shapes the quality of attention you receive. When the engagement is priced by the hour, the firm’s economics favor putting junior people on the work and having partners review. That’s how associates learn and how partners build scalable books of business. But you’re paying for that learning curve, and you often don’t know it until you see an invoice full of line items for research and “review of prior correspondence” from attorneys you don’t know.

What you’re buying is a set of outcomes. A cap table that ties out correctly when the round closes, or a term sheet for your Series A that doesn’t create problems when you raise your B. The value of those outcomes to your company is the same whether they take 40 hours to produce or 15.

Value-based pricing structures fees around the deliverable rather than the hours consumed producing it. The idea isn’t new, but interest has been increasing in recent years. Over half of surveyed firms now run hybrid billing models, and flat fees are the most common billing method among small firms with repeatable legal needs (Clio 2024, 2025).²

Under this model, there's no economic reason to staff a third-year associate on research that a senior attorney could resolve in a phone call, and no revenue benefit to a fourth round of internal review that doesn't change the document. The firm has an incentive to work efficiently. You get senior attention without paying for the overhead of a staffing pyramid.

What value-based pricing fixes…and what it doesn’t

That logic is sound, as far as it goes. But a pricing model only works as well as the agreement defining it, and most founders never scrutinize that agreement until something goes wrong.

Value-based pricing solves real problems. You know the cost before the work begins, which matters when you’re managing a seed-stage burn rate and every dollar has a board-approved purpose.

Your counsel is rewarded for efficiency and expertise rather than for taking longer. And you can call with a question without doing mental math about whether a 15-minute conversation just cost you $200.

Early data on the model's mechanics is directional. Firms billing flat fees collect payments nearly twice as fast and close matters 2.6 times faster than hourly-billed equivalents, and 71% of clients say they'd prefer a flat fee for their entire matter (Clio 2024, 2025).² The data is self-reported, but the direction is consistent across multiple years of the survey.

But value-based pricing is not self-executing. The specifics of the agreement determine whether it works, and the most common failure mode is scope ambiguity.

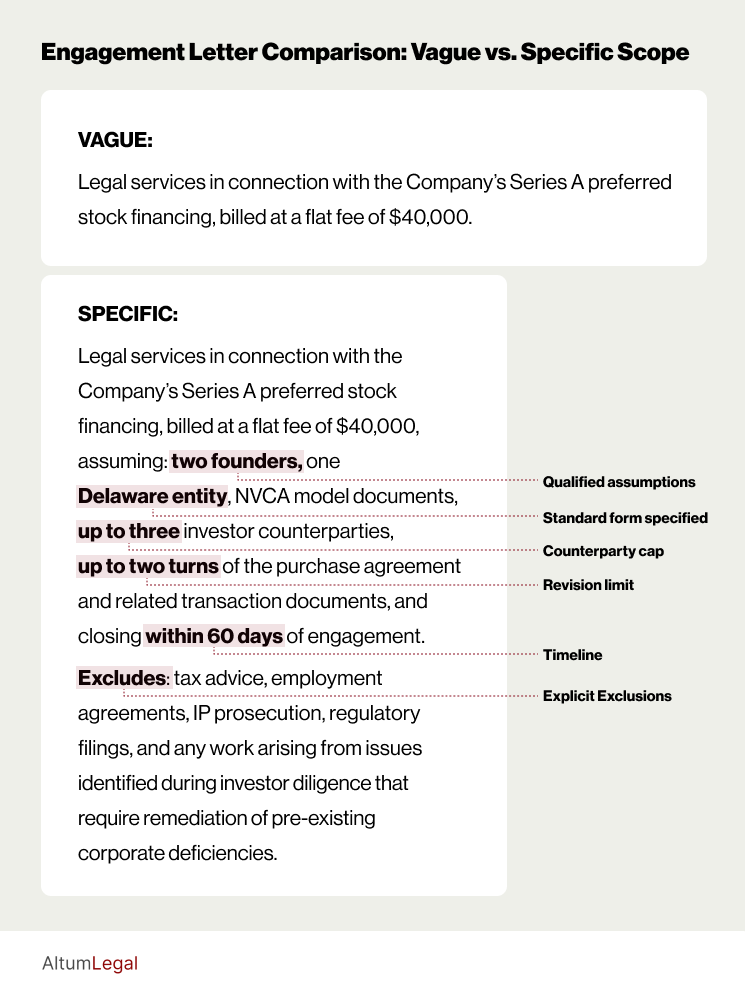

A flat fee is only as good as the scope definition behind it. If the engagement letter says “legal services in connection with the Company’s Series A preferred stock financing” and stops there, neither side knows what they’ve agreed to. How many investor counterparties? How many turns of the documents? Is the company on NVCA model forms, or does the lead investor’s counsel use proprietary drafts that require substantially more negotiation? What happens if diligence surfaces a pre-existing problem, like a missing founder IP assignment, that has to be resolved before the round can close?

If those variables aren't specified, the first time reality diverges from the unstated assumptions, both sides end up in a conversation that can easily turn contentious.

Some legal work genuinely resists fixed pricing at intake: a novel regulatory question where the research path is unknowable, or a contested negotiation where the number of turns depends on a counterparty you can’t control. For that work, a hybrid approach (flat fee for the defined scope, per-project quotes for the unpredictable parts) is often more honest than forcing everything into a single number.

There are also regulatory guardrails: in most jurisdictions, advance flat fees must be deposited in trust and withdrawn only as earned, which is why well-designed engagement letters tie fee milestones to specific phases of work rather than calendar dates.¹

None of this means value-based pricing is the wrong model. It means the engagement letter is where the model works or falls apart. Which raises a question most founders never think to ask.

How to read an engagement letter like an informed buyer

The question is, what happens when the work exceeds the scope?

Every other question worth asking about an engagement letter is a version of that one. Whether you’re evaluating an hourly proposal, a flat-fee quote, or a hybrid arrangement, the engagement letter determines what you’re paying for, what you’re not paying for, and what happens when reality doesn’t match the plan.

Most founders sign these the way they sign most contracts. They skim for the number at the bottom, check whether it’s in the range they expected and move on.

But at the first scope dispute the engagement letter becomes the only thing that matters. Here's what to look for.

Are the assumptions quantified? A well-scoped engagement letter specifies the variables that drive cost. For a Series A financing, that means: cap table complexity (how many outstanding SAFEs, convertible notes, option grants), number of investor counterparties, anticipated number of draft revisions, whether the deal uses standard forms or requires custom drafting, the expected diligence requirements, whether the investor will require a legal opinion, and expected timeline to closing.

If any of these are left open, the fee is an estimate, not a fixed price.

Are the exclusions as specific as the inclusions? The engagement letter should tell you what’s not covered with the same precision as what is covered. Standard carve-outs for a startup financing engagement include tax advice, securities filing fees, employment law matters, IP prosecution, and regulatory work.

If the letter only describes what the fee includes, you have no way to anticipate what will trigger additional charges.

Is there per-unit pricing for predictable expansions? The best engagement letters include language like: “Additional investor counterparty beyond three: $X per counterparty. $Y per side letter, and $Z for legal opinion.”

This prevents a full re-scoping conversation every time the deal gets slightly more complex than the original assumptions. It also signals that the firm has done enough of these deals to know where scope typically expands, which is itself a useful indicator of experience.

What triggers a scope change, and who controls it? This is where most engagement letters are thinnest and where the most money is at stake. A useful test, drawn from Patrick Lamb's framework for value-fee engagement letters:³ Was the issue or circumstance reasonably foreseeable when the engagement was scoped?

If it was foreseeable, Lamb argues, a change order requesting additional fees is not appropriate, because the firm should have accounted for it in the original price. An investor requesting one more turn of the purchase agreement is foreseeable in any financing. Your counsel should have built that into the scope.

A previously undisclosed co-founder emerging during diligence with an unsigned IP assignment is not foreseeable. That's a legitimate scope change.

The engagement letter should specify how additional work gets priced when it arises (a separate flat-fee quote is more transparent than reverting to hourly), and whether you have the right to decline the additional work and accept the risk.

Consider the difference between these two scope descriptions for the same Series A engagement:

Both letters quote the same fee for the same transaction.

Version A gives you a number. Version B gives you a shared understanding of what that number covers, which means you’ll also understand why when something falls outside it.

Version B’s exclusion for “remediation of pre-existing corporate deficiencies” is broad by design: in a messy diligence situation, that exclusion could cover a significant share of the work. That’s a reason to have a direct conversation about what it covers in practice before you sign, so neither side is surprised later.

What “value-based” actually means in practice

The founder from before had an information problem. The engagement letter she signed didn't give her enough detail to understand what she was paying for, what was excluded, or what would happen when the work expanded.

Value-based pricing doesn't mean the number is always lower. What it does mean is the price is legible. You understand what it reflects, what assumptions it rests on, and what happens when those assumptions change.

That's a higher standard than “we charge flat fees,” and it’s a more useful one.

The next time someone sends you an engagement letter, hourly or flat-fee or hybrid, ask what happens when the work exceeds this scope. If the answer is clear, specific, and reasonable for both sides, the pricing model is doing its job, even if the details still need negotiation.

If the answer is vague or missing entirely, “value-based pricing” is just a label.

¹ ABA Formal Opinion 505 (May 2023) holds that advance flat fees must be placed in a client trust account and withdrawn only as earned, regardless of how the fee is labeled. The practical solution is milestone-based structures with earning triggers tied to phases of work: initial analysis complete, documents drafted, negotiation concluded, closing finished. Both sides know when portions of the fee become earned, and the firm avoids the ethical risk of premature withdrawal.

² Specific adoption figures: 75% of solo firms and 65% of small firms use flat fees in some form (Clio 2025 Legal Trends Report); 54% of firms run hybrid hourly/flat-fee billing (Clio 2024). Data is self-reported and may skew toward firms using Clio's platform.

³ Patrick Lamb, "Prepping a Value-Fee Engagement Letter? Consider These 13 Issues First," ABA Journal, November 7, 2012. The foreseeability test appears in item 6 of Lamb's 13-issue checklist. Lamb also published two books on value fees: Alternative Fee Arrangements: Value Fees and the Changing Legal Market (2010) and Alternative Fees for Litigators and Their Clients (2014).

Sources: Clio 2024 and 2025 Legal Trends Reports (flat-fee adoption, collection speed, matter closure rates, and client billing preferences; self-reported data); ABA Formal Opinion 505, May 2023 (trust account requirements for advance flat fees); Patrick Lamb, "Prepping a Value-Fee Engagement Letter? Consider These 13 Issues First," ABA Journal, November 7, 2012 (value-fee engagement letter framework and change order standards).